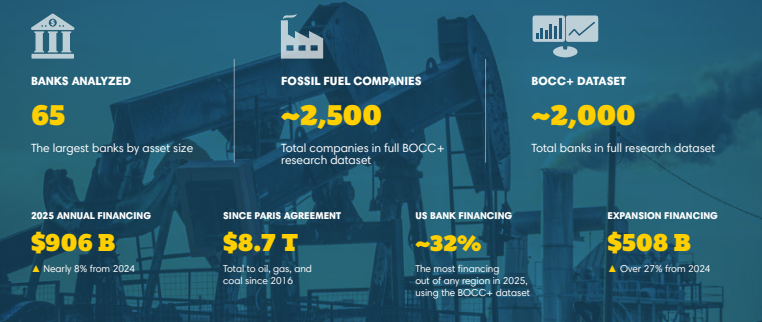

In a striking confirmation of the enduring role of fossil fuels in global finance, the world’s 65 largest banks committed a record $906 billion to oil, natural gas, and coal companies in 2025 — an 8% jump from $869 billion the year before. This marks the second straight year of rising fossil fuel financing after a brief dip tied to ESG commitments.

The data comes from the 17th annual Banking on Climate Chaos report by the Rainforest Action Network and partners. Since the 2015 Paris Agreement, these banks have funneled a staggering $8.7 trillion into the sector. U.S. institutions now account for 32% of the total (up from 28% in 2021), with JPMorgan Chase leading at $58.2 billion (up 12.5%), followed closely by Bank of America and Japan’s Mitsubishi UFJ Financial Group, each at $47 billion.

Just as this surge was taking shape, geopolitical reality delivered a brutal reminder of why energy security trumps abstract climate pledges. The 2026 Iran War triggered the effective closure of the Strait of Hormuz starting in early March. Iranian actions — including attacks on shipping and infrastructure — have stranded roughly 20% of global seaborne oil and a significant share of LNG exports. Brent crude spiked past $120 per barrel at points, and cumulative supply losses have already topped 1 billion barrels.

This is not a temporary blip. The crisis has exposed the fragility of Middle East-centric supply chains and is accelerating a structural shift: massive new spending and financing for exploration and production (E&P), pipelines, LNG terminals, and other infrastructure outside the Hormuz risk zone.

Diversification Away from Hormuz: The New Energy Security Playbook

Major oil and gas companies have responded with announcements and accelerated activity focused on assets far from the Persian Gulf. U.S. independents and majors are ramping up Permian and other shale plays, with frac spreads in the basin up 20% in recent weeks as already-drilled wells come online faster.

Producers outside the Gulf — particularly in the Americas — are seeing clear tailwinds. U.S. LNG exporters stand to gain as buyers seek non-Gulf supplies, while Canadian oil sands and pipeline expansions to the West Coast are gaining fresh momentum amid security-driven demand.

Pipeline diversification is also surging. Saudi Arabia is eyeing expansion of its East-West pipeline (bypassing Hormuz to the Red Sea), while the UAE is fast-tracking capacity increases via the Habshan-Fujairah route and planning a doubling by 2027.

China is leaning harder into Russian and Central Asian pipelines (Power of Siberia expansions that have not been approved yet, and other new deals) to reduce seaborne reliance.

Global LNG supply growth is being redirected: new projects outside the Gulf (U.S., Canada, East Africa, and others) are moving forward to fill the gap left by Qatari and other Gulf disruptions. Wood Mackenzie notes that persistent uncertainty will support investments in LNG outside the Gulf while reinforcing coal and renewables in some Asian and European markets — but the immediate financing wave favors secure, deliverable hydrocarbons.

Coal’s Quiet Comeback Under the Energy Security Banner

Even coal — long the poster child of ESG divestment — is seeing more open consideration. With LNG and oil flows disrupted, some utilities and governments are prioritizing reliable baseload power. Banks have not slammed the door; several continue to finance coal-related activities, and policy shifts in places like the U.S. (emergency orders to keep plants online, funding to delay retirements) signal that energy security is now the dominant lens.

The Banking on Climate Chaos data itself shows coal still receiving significant flows within the $906 billion total. In an era of $100+ oil and strained gas supplies, the narrative has flipped from “phase out at all costs” to “keep the lights on and industries running.” Financing is rolling not into ESG theater but into pragmatic energy security.

Renewables, Wind, Solar, and Hydrogen: Headwinds Intensify

Meanwhile, investment trends in wind, solar, and hydrogen are cooling. Global clean energy spending remains substantial (IEA data shows $2.2 trillion in 2025 vs. $1.1 trillion for fossils), but growth has slowed markedly in key markets. U.S. wind and solar investments fell sharply in the first half of 2025 amid policy changes, with some pipelines contracting 18% or more.

Hydrogen projects have seen cancellations and delays; absolute spending remains tiny (under $30 billion globally) and heavily policy-dependent.

Higher financing costs in a volatile environment hit capital-intensive renewables harder than established fossil infrastructure. Banks’ own data reflects the lag: they still allocate far more to fossils than to low-carbon alternatives.

Make no mistake – The world spent over 10 trillion dollars on wind and solar to only have gained 3% energy – Secretary Chris Wright.

Secretary Chris Wright is spot on, and on the Energy News Beat podcast with a Nuclear expert, Todd Royal, they did a little exercise in real time. If we took the 10 trillion spent on wind and solar and spent it on nuclear, the world would be a different place. The US currently has 96 reactors, with one coming on line this year and potentially another next year for 98 reactors. We could have added another 174 reactors to replace all forms of main power plants, and still have 1,700 reactors to spread around the world. We truly would have been Net Zero. The world would still need oil and gas, but a significant reduction.

The Bottom Line: Energy Security Is Driving the Capital Allocation

The $906 billion fossil fuel financing figure for 2025 was already locked in before the full scale of the Hormuz crisis became clear. The Iran War has now supercharged the case for more of the same — but redirected toward secure, non-chokepoint assets. Exploration, production, pipelines, LNG terminals, and even coal infrastructure are seeing renewed capital flows precisely because they deliver reliable energy when geopolitics turns ugly.

ESG-era rhetoric has not disappeared, but the market and policymakers are voting with dollars for energy security first. The world’s biggest banks, oil companies, and governments are aligning capital accordingly.

- OilPrice.com article (primary source): https://oilprice.com/Latest-Energy-News/World-News/Worlds-65-Biggest-Banks-Pumped-906-Billion-Into-Fossil-Fuels-in-2025.html (published June 9, 2026)

- Banking on Climate Chaos 2026 Report (full PDF and data): https://www.ran.org/wp-content/uploads/2026/06/BOCC_2026_vFINAL-1.pdf and https://www.bankingonclimatechaos.org/

- IEA World Energy Investment 2025 Executive Summary: https://www.iea.org/reports/world-energy-investment-2025/executive-summary

- Wikipedia: Economic impact of the 2026 Iran war (Hormuz closure details): https://en.wikipedia.org/wiki/Economic_impact_of_the_2026_Iran_war

- Wood Mackenzie analysis on Hormuz scenarios and LNG/coal/renewables impacts: https://www.woodmac.com/press-releases/strait-of-hormuz-closure-risks-greatest-global-energy-supply-shock-in-decades/

- Reuters/others on China diversification and pipelines: https://www.reuters.com/graphics/IRAN-CRISIS/CHINA-OIL/egpbeormkvq/

- Atlantic Council on energy policy shifts from Iran war: https://www.atlanticcouncil.org/blogs/energysource/how-the-iran-war-could-shift-energy-policies-around-the-world/

- BNEF on bank financing ratios: https://about.bnef.com/insights/finance/bank-financing-shows-little-progress-on-climate-goals-five-things-to-know/

- Deloitte 2026 Renewable Energy Industry Outlook (U.S. wind/solar slowdown): https://www.deloitte.com/us/en/insights/industry/renewable-energy/renewable-energy-industry-outlook.html

- Additional context from CSIS, Brookings, and industry reports on U.S./non-Gulf production responses.

This article reflects verified data as of June 9, 2026. Energy markets remain fluid; developments in the Iran conflict will continue to shape financing flows.

The post World’s 65 Biggest Banks Pumped $906 Billion Into Fossil Fuels in 2025. The Iran War will escalate exploration and production, pipelines, and energy security spending and financing. appeared first on Energy News Beat.