This was a fun joint podcast and will go out on both channels!

In an era of unprecedented geopolitical tension and energy market volatility, Stu Turley of the Energy Newsbeat podcast sits down with Trisha Curtis, CEO of the Petro Nerds podcast, to dissect the forces reshaping global energy markets and international power dynamics. From Iran’s desperate gambit to control the Strait of Hormuz to China’s calculated investments in coal-to-oil synthesis, this conversation reveals how energy—not ideology or military might alone—is the true currency of geopolitical leverage.

We challenge conventional market wisdom, expose the hidden costs of net-zero policies, and make a compelling case that the United States possesses unprecedented energy advantages that policymakers and analysts have catastrophically underestimated. With Europe in energy decline, China preparing for conflict through energy resilience, and the Middle East in flux, this episode serves as a masterclass in understanding why energy security is national security, and why the decisions made today will determine which nations thrive and which fade into irrelevance.

Check out the PetroNerds at https://www.youtube.com/@petronerds633

Connect with Trisha on LinkedIn https://www.linkedin.com/in/trisha-curtis-petronerds/

1. Global Oil Market Volatility & Strait of Hormuz Crisis

The hosts discuss the unprecedented market volatility throughout the year, particularly focusing on the Strait of Hormuz and Iran’s actions. They analyze how Iran’s attacks on shipping and infrastructure represent desperation rather than strength, as alternative pipelines and routes are being developed by Saudi Arabia and the UAE to bypass Iranian control.

2. Strategic Petroleum Reserve (SPR) Management

A significant focus on how the U.S. and China are using their SPRs differently. Secretary Chris Wright is praised for using the SPR as a loan (requiring repayment) rather than as a permanent release, thereby avoiding budget cycle issues. We note that this strategy received insufficient market coverage. It is, if managed correctly, it will help refill the SPR.

Energy markets are flashing warning signs as U.S. petroleum product exports remain near record highs while domestic inventories tighten amid escalating geopolitical risks in the Middle East. Veteran energy analyst Anas Alhajji (@anasalhajji) highlighted these concerns in his July 9, 2026, Daily Energy Report on X and Substack, posing a series of pointed questions that cut straight to the heart of U.S. energy security. We will reach out to Dr. Alhajji and see about getting him on the Energy News Beat podcast. We highly recommend subscribing to X and his Substack.

The lead question stands out: “How long can strong U.S. petroleum product exports continue before they cause significant domestic inventory shortages and price spikes?”Alhajji also asks about the expected impact of the Hormuz crisis and SPR releases on U.S. diesel exports and WTI crude prices, among other timely issues.

Record Exports Depleting U.S. Product Inventories

U.S. exports of diesel, propane, gasoline, and jet fuel have surged to or near all-time highs, driven by strong overseas demand. This comes as the Iran conflict escalates, and Russia has halted some diesel exports.

According to Alhajji’s analysis, record fuel exports have pushed U.S. diesel and gasoline stockpiles to their lowest seasonal levels in years. Both gasoline and distillate (diesel) inventories sit below the bottom of their five-year average range.

Key question from Alhajji: Will these elevated export levels continue? Could the U.S. see record declines in product inventories that push prices to new highs? What will be the impact on crude oil prices—particularly WTI—if product inventories keep falling?

These are not hypothetical concerns. Tight product inventories combined with high export volumes create a classic setup for domestic shortages and price spikes if supply chains face any additional stress.SPR at Multi-Decade Lows: Approaching Critical Thresholds

Cross-checking with official data shows the U.S. Strategic Petroleum Reserve (SPR) has been drawn down sharply as part of responses to global supply disruptions.

Latest EIA data (week ending July 3, 2026):

SPR crude oil stocks: 319.5 million barrels (down 6.2 million barrels from the prior week’s 325.7 million barrels).

This is the lowest level since 1983.

There is no strict current legislative “congressional bottom” for the SPR. However, analysts and officials reference several key thresholds:

- Estimated minimum operating level: ~300 million barrels.

- Emergency floor to help prevent salt cavern collapse: ~250 million barrels.

- Previously certified SecDef floor (tied to the 172 million barrel release authorization): 243 million barrels.

At the recent draw rate of ~6.2 million barrels per week (~0.89 million barrels per day):Reaching the ~300 million barrel operational minimum:

- Roughly 20 days (about 19.5 million barrels remaining).

- Reaching the ~250 million barrel emergency floor: Roughly 70 days.

- Reaching the 243 million barrel certified floor: Roughly 76 days.

These are rough linear estimates—actual draw rates can vary, slow as caverns empty, or change due to policy decisions. Further releases would accelerate the timeline and heighten risks to long-term energy security.

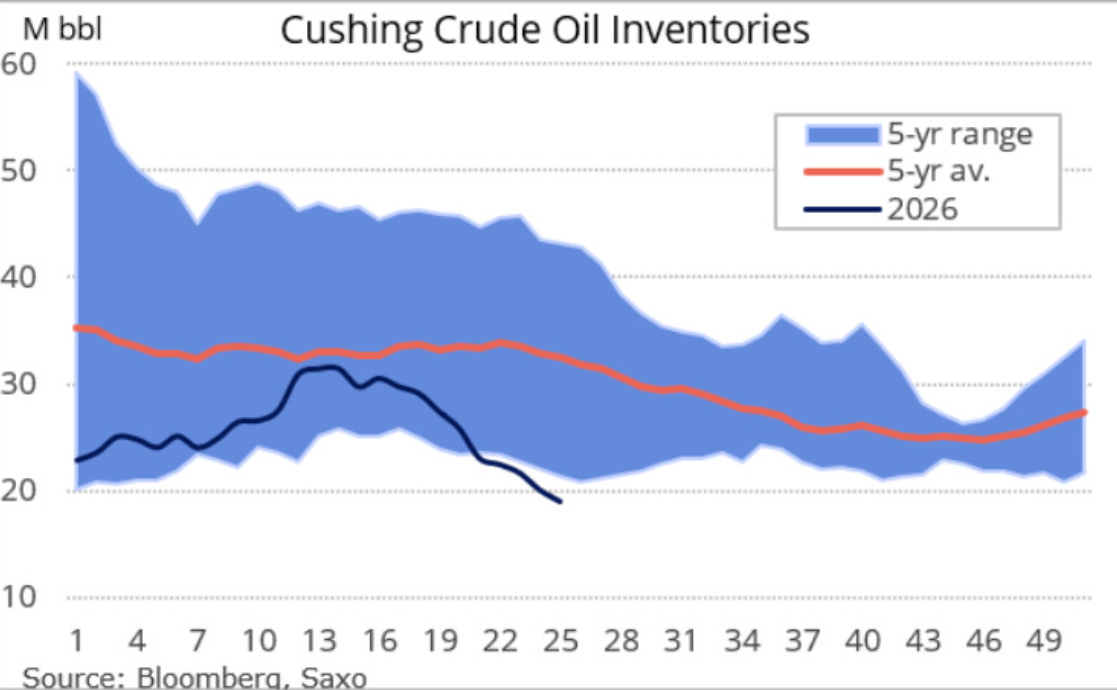

Cushing Inventories Remain Critically Low

At the key WTI pricing and delivery hub in Cushing, Oklahoma, commercial crude inventories are also under pressure.

Latest EIA data (week ending July 3, 2026): Cushing stocks stood at 19.6 million barrels.

This level is near or slightly below the widely cited operational floor of around 20 million barrels. Below this threshold, operational challenges increase (difficulty pulling oil from tanks, quality issues from water/sediment).

Has Cushing’s inventory increased? Yes, modestly in recent weeks. It bottomed around 18.96 million barrels in mid-June before rising to the 19.6–19.7 million barrel range. However, it remains extremely tight historically and vulnerable to further draws from strong export demand and refining activity.

3. U.S. Oil & Natural Gas Production

Discussion of America’s impressive production capacity—nearly 14 million barrels per day of crude oil and 136 billion cubic feet per day of natural gas. The hosts emphasize that the U.S. has significant leverage in global energy markets that isn’t being properly appreciated or communicated.

4. China’s Energy Strategy & Geopolitical Implications

Extensive analysis of China’s energy stockpiling, coal-fired power generation dominance (more than the U.S. total capacity), and investments in coal-to-oil synthetic manufacturing. The hosts interpret China’s 2026 coal-to-oil investments as preparation for potential conflict.

5. European Energy Crisis & Decline

Critical examination of Europe’s energy policy failures, particularly the UK and Germany’s abandonment of coal and nuclear power. The hosts highlight how net-zero policies have made Europe dependent on Russian LNG and created energy security vulnerabilities.

6. Electricity Grid Reliability & Cost Issues

Detailed analysis showing that wind and solar installations increase electricity costs without improving reliability. The hosts present data showing blue states have 38% higher electricity prices than red states, correlating directly with renewable energy policies. They argue that baseload power (coal, natural gas, nuclear) is essential.

7. ESG & Net-Zero Policy Criticism

Strong critique of ESG metrics and net-zero commitments by major oil companies, arguing these policies increase costs without environmental benefit and represent a form of control rather than genuine sustainability.

8. U.S. Manufacturing & Supply Chain Resilience

Discussion of reshoring manufacturing and the importance of controlling the entire energy value chain—from crude extraction through plastics manufacturing—to reduce dependence on China and create a more resilient economy.

9. NATO, Defense Spending & Geopolitical Realignment

Analysis of NATO discussions, with criticism of European countries (particularly Spain) for insufficient defense spending and energy investment. Discussion of new trading blocs forming around the U.S., Saudi Arabia, UAE, Russia, India, and Japan.

I covered this in the article Europe’s Industrial Death Spiral due to Net Zero Energy may not be recoverable.

The EU cannot remilitarize due to its deindustrialization and its looming fiscal collapse. All due to Net Zero and the initiation of the Green Energy Wealth transfer.

10. LNG Market Dynamics

Analysis of Qatar’s LNG production disruptions and the broader natural gas market, including how Iran’s attacks on LNG vessels represent attempts to control energy flows and how alternative infrastructure (floating LNG, pipelines) may bypass traditional chokepoints.

The overarching theme is that energy security is fundamental to national security and economic prosperity, and current Western policies prioritizing net-zero over reliable, affordable energy are strategically disadvantageous compared to competitors like China.

QatarEnergy has paused its aggressive ramp-up plans at the Ras Laffan LNG complex following a recent tanker attack in the Strait of Hormuz, prioritizing security over speed. This decision delays the critical LNG supply that the market had been counting on for the upcoming winter season.

According to market analyst Jack Prandelli (@jackprandelli), QatarEnergy had previously targeted 50% of Ras Laffan capacity within a month, 80% within two months, and “normal production within weeks.” Following the latest security incident, the company is now running at minimum safe operations, with fewer vessels transiting the Hormuz Strait until tensions ease. Approximately 12-13 million tonnes per annum (mtpa) of capacity was already offline from earlier attacks in 2026.

This comes on top of significant damage from Iranian attacks on Ras Laffan in March 2026, which knocked out roughly 17% (about 12.8 mtpa) of Qatar’s total LNG export capacity for an estimated 3–5 years. Qatar’s overall LNG production capacity stands at approximately 77 mtpa.

Impact on EU and Asian Markets

The slowdown removes expected near-term supply relief and tightens the global LNG balance just as Europe and Asia enter winter positioning season. Spot LNG prices in both regions had eased on hopes of rising Qatari flows; the pause now reintroduces upward pressure, adding a premium to Atlantic Basin (Europe-focused) and Pacific Basin alternatives.

Europe relies heavily on LNG imports following the sharp reduction in Russian pipeline gas since 2022. Any delay in Qatari supply heightens competition with Asia for available cargoes. Asian buyers, traditionally major offtakers of Qatari LNG, will bid aggressively, potentially diverting volumes away from Europe and supporting higher prices.

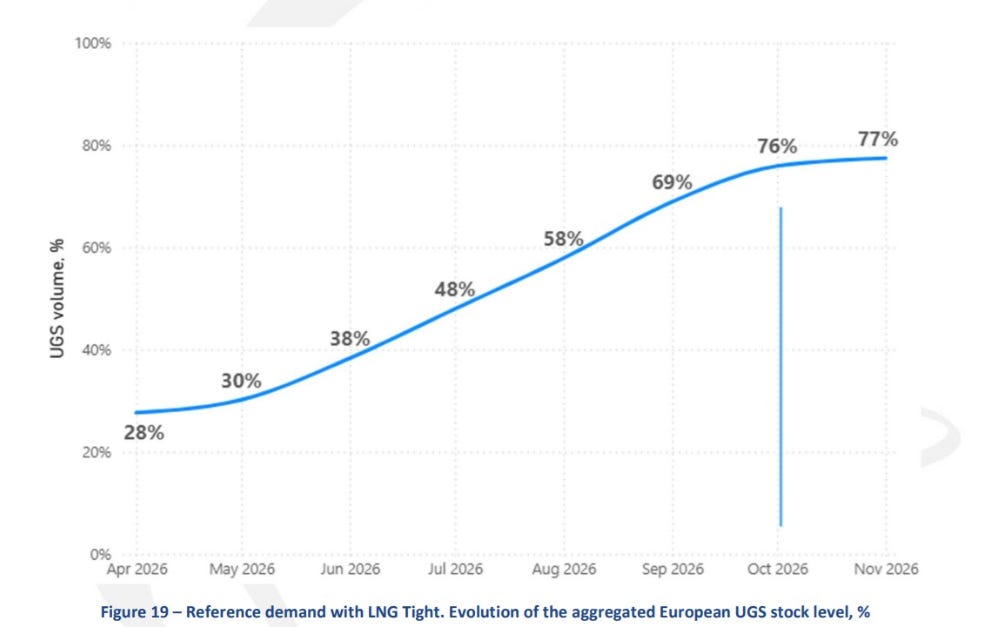

EU Gas Storage Levels and Summer Filling Challenges

EU natural gas storage currently sits at approximately 50–51% full as of early July 2026 (around 565–572 TWh), one of the lower levels for this time of year in recent history.

en.

This low starting point for the injection season (following a relatively cold winter) means Europe needs strong LNG inflows this summer to reach even the relaxed 80% target by November 1. High spot prices driven by tighter global supply are already disincentivizing aggressive storage injections.

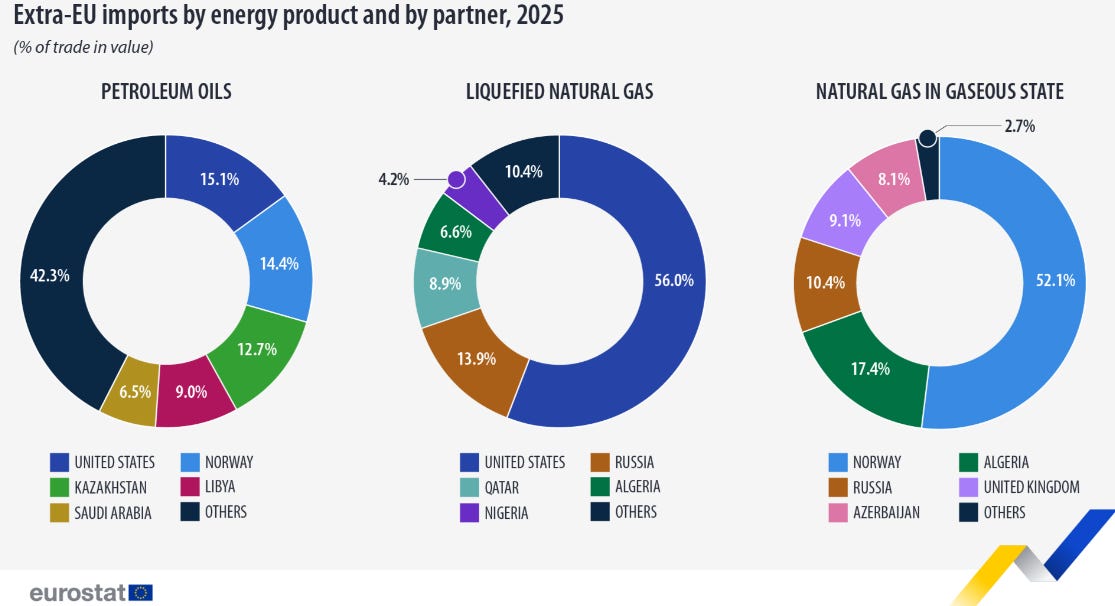

Russia’s ongoing role: Despite diversification efforts and the EU’s phase-out plans, Russia still accounted for around 12–14% of EU gas imports in 2025 (pipeline via TurkStream and some LNG). In 2025 data:

LNG imports: US ~56%, Russia ~14%, Qatar ~9%.

Pipeline gas: Norway is dominant (~52%), followed by Algeria (~17%), Russia (~10%).

The EU adopted regulations in early 2026 to prohibit Russian pipeline and LNG imports (with transition periods), but volumes via existing routes (e.g., TurkStream to Hungary and Slovakia) have persisted or even increased in early 2026. Full bans on Russian LNG are slated for 2027 in some cases.

Implications for Consumers and Businesses in the EU

Higher and more volatile gas prices will directly translate into elevated electricity and heating bills for households this winter. Energy-intensive industries (chemicals, fertilizers, steel, glass, and manufacturing) face squeezed margins, potential production cuts, or relocation pressures.

With Russian gas being phased out and Qatari supply delayed, Europe’s reliance on more expensive spot LNG and alternative suppliers (primarily US LNG) increases costs. Businesses may pass on higher energy expenses to consumers through inflation in goods and services. Energy security concerns could intensify if winter weather turns colder than expected or if further Middle East disruptions occur.

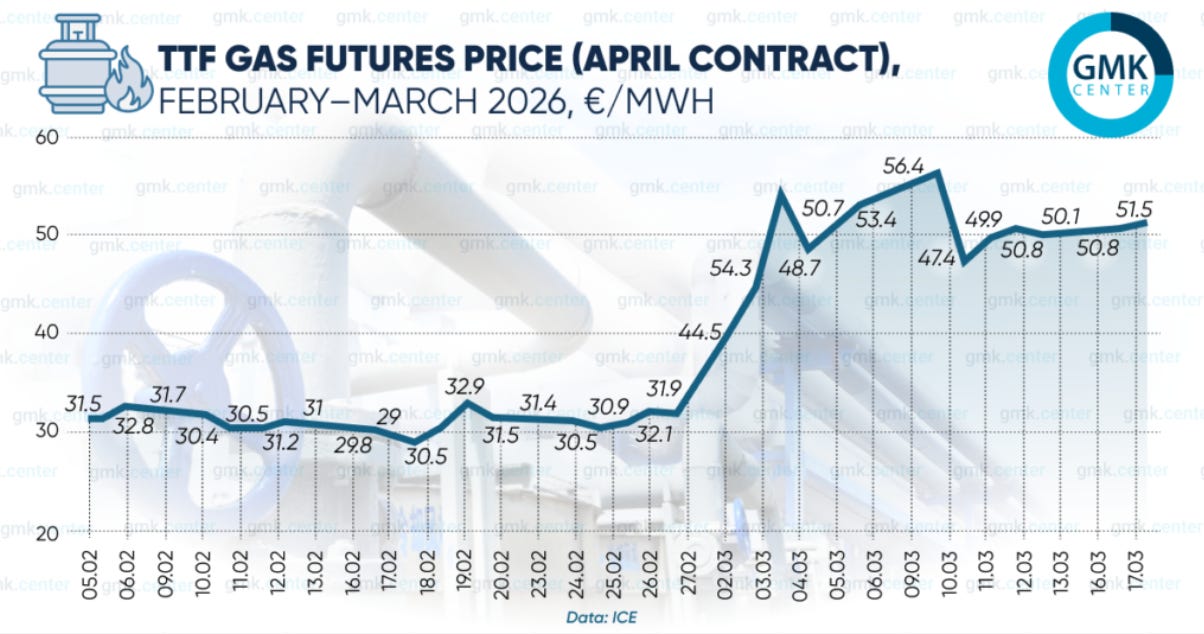

Market Context and Price Reaction

European TTF gas prices have shown significant volatility in 2026 amid Middle East tensions, with sharp spikes earlier in the year following initial Qatar disruptions.

The EU adopted regulations in early 2026 to prohibit Russian pipeline and LNG imports (with transition periods), but volumes via existing routes (e.g., TurkStream to Hungary and Slovakia) have persisted or even increased in early 2026. Full bans on Russian LNG are slated for 2027 in some cases.

Implications for Consumers and Businesses in the EU

Higher and more volatile gas prices will directly translate into elevated electricity and heating bills for households this winter. Energy-intensive industries (chemicals, fertilizers, steel, glass, and manufacturing) face squeezed margins, potential production cuts, or relocation pressures.

With Russian gas being phased out and Qatari supply delayed, Europe’s reliance on more expensive spot LNG and alternative suppliers (primarily US LNG) increases costs. Businesses may pass on higher energy expenses to consumers through inflation in goods and services. Energy security concerns could intensify if winter weather turns colder than expected or if further Middle East disruptions occur.

Market Context and Price Reaction

European TTF gas prices have shown significant volatility in 2026 amid Middle East tensions, with sharp spikes earlier in the year following initial Qatar disruptions.

This will be more in line with a new series covering the global energy policies and insights from Trisha.

We are about to see a massive global build-out of energy security by establishing global choke points. The Energy Boom is starting, and an AI bubble may be forming as the realization sets in that only AI that is useful and can be held accountable will be funded. Data Centers that have power and an income stream will be built.

Doing Data Centers Done Right is critical. Not on Farmland, with accountability, or increasing consumer energy. We can do this, and the world is healing.

That is where Jon Brewton and Data2 play into the mix.

Matt Lozack, Cofounder and CEO, Aalo Atomics, on the Energy News Beat Podcast Next Week. They just had a new reactor hit their targets, and this is HUGE.

A shout-out to Steve Reese and the Reese Energy Consulting group for sponsoring the Podcast https://reeseenergyconsulting.com/.

Data2 if you have any business systems, can you trust A? Well, they have the patent on validation. . https://data2.zoholandingpage.com/energy

And we have WellDatabase rolling in as a new sponsor. https://welldatabase.com/

The post The Future of the Oil and Gas Markets – Special Joint Podcast with Trisha Curtis, PetroNerds appeared first on Energy News Beat.