The United Arab Emirates (UAE) has announced its withdrawal from the Organization of the Petroleum Exporting Countries (OPEC) and the broader OPEC+ alliance, effective May 1, 2026—marking the end of nearly 60 years of membership since 1967.

This move strips OPEC of its third-largest producer and delivers a significant blow to the cartel’s ability to coordinate global oil supply and influence prices, especially amid the ongoing Iran war and disruptions in the Strait of Hormuz.

As highlighted in a recent NewsMax segment featuring Carl Higbie, the UAE’s exit—combined with Saudi Arabia’s capacity—positions the United States for greater global energy dominance. If Saudi Arabia and the UAE begin maximizing output (bypassing Hormuz constraints via Red Sea pipelines), Iran’s oil becomes “completely irrelevant” in the market.

Why the UAE Left OPEC

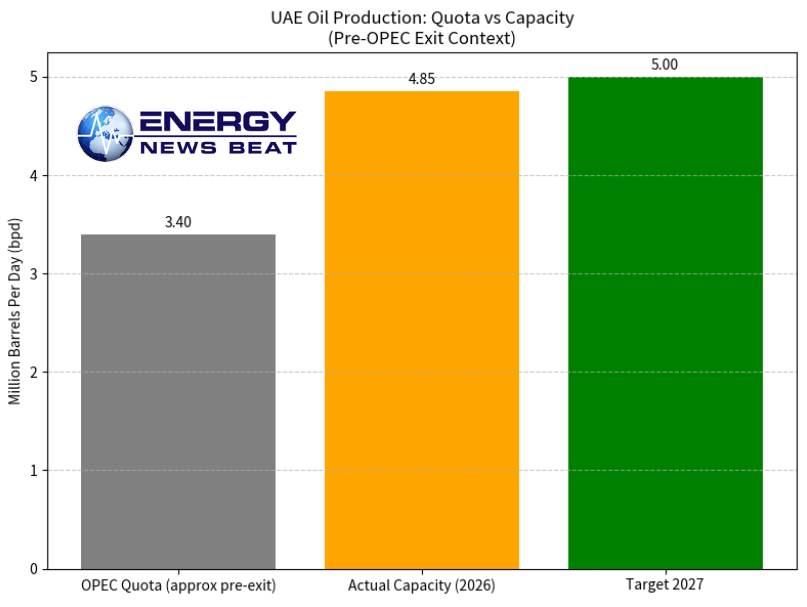

The decision stems from long-standing frustrations with OPEC+ production quotas that constrained the UAE well below its true potential. The UAE’s maximum sustainable capacity stands at approximately 4.85 million barrels per day (bpd), with ambitions to reach 5 million bpd by 2027 through investments by Abu Dhabi National Oil Company (ADNOC). However, OPEC+ quotas typically limited output to around 3–3.5 million bpd (and lower in recent war-disrupted months).

UAE Energy Minister Suhail Al Mazrouei stated the exit reflects the country’s “long-term strategic and economic vision,” prioritizing national interests, production flexibility, and meeting global demand without cartel obligations. Geopolitical factors—including reported Iranian drone and missile attacks during the current conflict and tensions with Saudi Arabia (OPEC’s de facto leader)—accelerated the move.

The UAE plans a “gradual and measured” increase in production aligned with market conditions, freeing it from the group’s collective decisions.

UAE Oil Production: Quota vs. Capacity (Pre-Exit Context)

Verification of Gulf Oil Production: Charts and Data

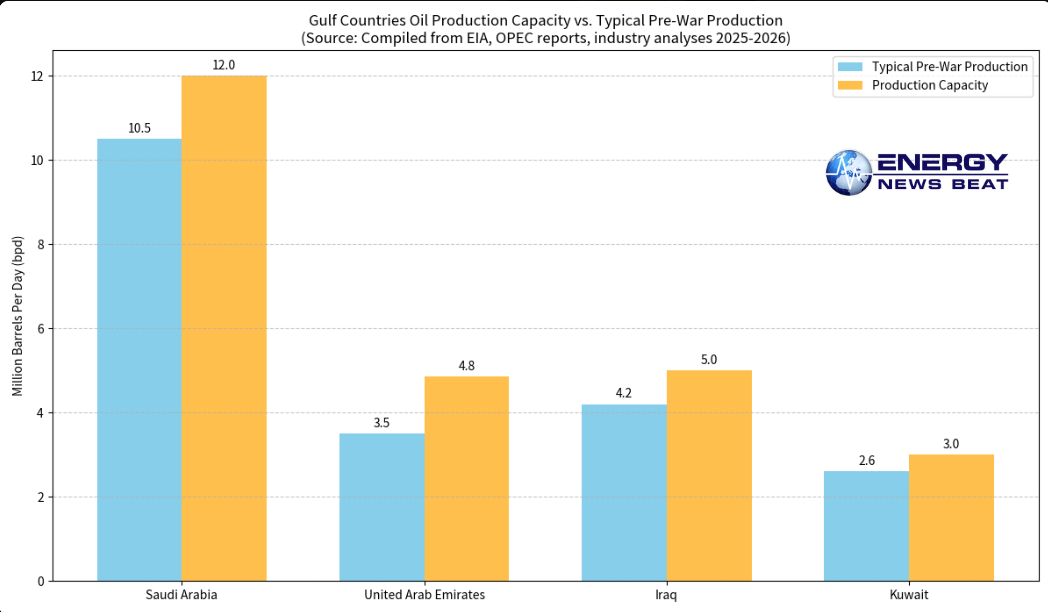

To verify the scale of this shift, here is a clear look at major Gulf producers. Pre-Iran war figures (approximate 2025/early 2026 baseline) show significant spare capacity in the region—particularly for the UAE—that OPEC+ quotas had previously capped. War-related disruptions (Hormuz closure, field shut-ins) have already slashed output across the Gulf, but the UAE’s exit unlocks independent ramp-up potential once logistics stabilize.

Gulf Countries Oil Production Capacity vs. Typical Pre-War Production (Million bpd)

Key notes from data (EIA/OPEC/industry sources): Saudi Arabia: ~10.5M bpd typical production / 12M+ bpd capacity (heavily curtailed recently to ~7.8–8M bpd).

UAE: ~3.5M bpd typical / 4.85M bpd capacity (target 5M by 2027).

Iraq: ~4.2M bpd typical / ~5M bpd capacity.

Kuwait: ~2.6M bpd typical / ~3M bpd capacity.

The UAE’s exit removes a key spare-capacity player from OPEC+ coordination, potentially allowing faster supply growth once Hormuz-related issues ease (alternative pipelines like the UAE’s to Fujairah and Saudi’s East-West line provide bypass options).

“If just [Saudi Arabia and United Arab Emirates] start maxing out their production, which they can do by the end of this year, Iran’s oil market is completely irrelevant.”@CarlHigbie explains how the UAE leaving OPEC puts the United States in the position for global energy… pic.twitter.com/cKCUO5J6MI

— NEWSMAX (@NEWSMAX) April 29, 2026

Global Impact on Oil Markets

OPEC (now down to 11 members) and OPEC+ lose meaningful leverage over roughly 4% of global crude supply and significant spare capacity. Analysts describe this as “the beginning of the end” for the cartel’s unified front, risking disarray, price volatility, and even internal price wars if Saudi Arabia responds aggressively to UAE output growth.

Short-term: Limited immediate relief due to ongoing Iran war disruptions (Hormuz choke point affecting ~20% of global oil transit). Oil prices have spiked above $100–110/bbl amid the crisis.

Long-term: Downward pressure on prices as the UAE (and potentially others) ramps production freely. This could stabilize markets, benefit consumers, and reduce cartel influence—aligning with views of enhanced U.S. energy positioning through abundant, diversified supply.

Specific Impact on China and the Dark Fleet

China, the world’s top oil importer, has heavily relied on discounted Iranian (and Russian) crude delivered via the “dark fleet” or shadow fleet of tankers that evade Western sanctions. Iran’s exports—largely funneled to China—have already been disrupted by the war, forcing higher costs and logistical risks.The UAE’s exit changes the equation: More legitimate, flexible supply from a trusted Gulf partner competes directly with sanctioned barrels.

China could shift purchases to open-market UAE crude (already a major supplier), reducing dependence on risky dark-fleet routes.

This represents a significant blow to the shadow fleet’s economics and Iran’s revenue stream, as cheaper, sanction-free alternatives become available in greater volume.

Analysts note this could accelerate China’s pivot away from illicit supply chains, especially if the UAE ramps up exports (potentially in yuan settlements amid broader geopolitical shifts). Combined with electrification trends already curbing China’s oil demand growth, the net effect pressures high-cost sanctioned oil flows.

Broader Implications and Outlook

This is a historic realignment in global energy geopolitics. The UAE asserts independence as a commerce/finance/energy hub (Dubai and Abu Dhabi), while weakening OPEC+ cohesion at a moment of historic energy shock. For the U.S., it reinforces energy dominance narratives by flooding potential supply and diminishing adversarial leverage (Iran, Russia via OPEC+).

Markets will watch the UAE’s post-May 1 actions closely. While immediate effects are muted by the Iran conflict, the long-term trajectory points to a more fragmented, flexible, and potentially lower-price oil landscape.

Key notes from data (EIA/OPEC/industry sources): Saudi Arabia: ~10.5M bpd typical production / 12M+ bpd capacity (heavily curtailed recently to ~7.8–8M bpd).

UAE: ~3.5M bpd typical / 4.85M bpd capacity (target 5M by 2027).

Iraq: ~4.2M bpd typical / ~5M bpd capacity.

Kuwait: ~2.6M bpd typical / ~3M bpd capacity.

The UAE’s exit removes a key spare-capacity player from OPEC+ coordination, potentially allowing faster supply growth once Hormuz-related issues ease (alternative pipelines like the UAE’s to Fujairah and Saudi’s East-West line provide bypass options).

Global Impact on Oil Markets

OPEC (now down to 11 members) and OPEC+ lose meaningful leverage over roughly 4% of global crude supply and significant spare capacity. Analysts describe this as “the beginning of the end” for the cartel’s unified front, risking disarray, price volatility, and even internal price wars if Saudi Arabia responds aggressively to UAE output growth.

Short-term: Limited immediate relief due to ongoing Iran war disruptions (Hormuz choke point affecting ~20% of global oil transit). Oil prices have spiked above $100–110/bbl amid the crisis.

Long-term: Downward pressure on prices as the UAE (and potentially others) ramps production freely. This could stabilize markets, benefit consumers, and reduce cartel influence—aligning with views of enhanced U.S. energy positioning through abundant, diversified supply.

Specific Impact on China and the Dark Fleet

China, the world’s top oil importer, has heavily relied on discounted Iranian (and Russian) crude delivered via the “dark fleet” or shadow fleet of tankers that evade Western sanctions. Iran’s exports—largely funneled to China—have already been disrupted by the war, forcing higher costs and logistical risks.

The UAE’s exit changes the equation: More legitimate, flexible supply from a trusted Gulf partner competes directly with sanctioned barrels.

China could shift purchases to open-market UAE crude (already a major supplier), reducing dependence on risky dark-fleet routes.

This represents a significant blow to the shadow fleet’s economics and Iran’s revenue stream, as cheaper, sanction-free alternatives become available in greater volume.

Analysts note this could accelerate China’s pivot away from illicit supply chains, especially if the UAE ramps up exports (potentially in yuan settlements amid broader geopolitical shifts). Combined with electrification trends already curbing China’s oil demand growth, the net effect pressures high-cost sanctioned oil flows.

Broader Implications and Outlook

This is a historic realignment in global energy geopolitics. The UAE asserts independence as a commerce/finance/energy hub (Dubai and Abu Dhabi), while weakening OPEC+ cohesion at a moment of historic energy shock. For the U.S., it reinforces energy dominance narratives by flooding potential supply and diminishing adversarial leverage (Iran, Russia via OPEC+).

Markets will watch the UAE’s post-May 1 actions closely. While immediate effects are muted by the Iran conflict, the long-term trajectory points to a more fragmented, flexible, and potentially lower-price oil landscape.

We will cover this on the Energy News Beat Stand Up today, and we recommend watching NewsMax and Carl Higbie.

Appendix: Sources and Links

- NewsMax X Post (Carl Higbie segment): https://x.com/NEWSMAX/status/2049279298427617708

- AP News: “UAE will leave OPEC in a blow to the oil cartel” – https://apnews.com/article/opec-united-arab-emirates-leaving-cartel-4966108c3fafacb67181152216deda14

- Reuters: “UAE leaves OPEC and OPEC+ in major blow…” – https://www.reuters.com/markets/commodities/uae-says-it-quits-opec-opec-statement-2026-04-28/

- Al Jazeera: “What are OPEC and OPEC+, and why has the UAE quit?” – https://www.aljazeera.com/news/2026/4/28/what-are-opec-and-opec-and-why-has-the-uae-quit

- BBC: “United Arab Emirates to quit oil cartel Opec” – https://www.bbc.com/news/articles/cj4pxwlr52yo

- Atlantic Council / The Conversation: Analyses on long-term divergence and Gulf realignment.

- Oil production data: Compiled from EIA (eia.gov), OPEC monthly reports, Rystad Energy, and industry updates (e.g., ADNOC capacity targets). Charts generated from these verified figures.

- Additional context: CNN, Washington Post, Axios, Fox Business, Bloomberg (April 28–29, 2026 coverage).

Energy News Beat – Delivering unbiased, data-driven energy intelligence.

Check out the Energy News Beat Substack: https://theenergynewsbeat.substack.com/

The post Why did the UAE leave OPEC, and what is the Global Impact appeared first on Energy News Beat.