As a record armada of crude oil tankers steams toward the U.S. Gulf Coast to load American barrels—171 vessels en route in April 2026, with 28 VLCCs already fixed for May loadings alone—another surge is unfolding downstream. U.S. crude cargoes transiting the Panama Canal are now exceeding 200,000 barrels per day (bpd) in the first half of April, approaching a four-year high last seen in July 2022.

This outbound flow directly ties into the inbound tanker fleet highlighted in our earlier report, “Tanker Fleet Knocking at the Gulf of America, but What Are They Buying and for Whom?” The same light, sweet U.S. crude grades prized by global refiners—primarily from Gulf Coast hubs like Houston, Beaumont, and Corpus Christi—are now moving rapidly through the Panama Canal en route to Asia.

Key Details on Tanker Activity and Cargo

Volume: More than 200,000 bpd of U.S. oil cargoes (overwhelmingly crude) via the Panama Canal in early April 2026, per maritime intelligence firm Kpler Ltd. This marks the strongest showing for this specific route in nearly four years.

Number of Tankers: While exact current counts are not publicly broken out, the volume spike reflects a clear uptick in medium-sized crude tankers. In March 2026 alone, at least three vessels were confirmed on this route, signaling the start of the current surge.

Vessel Types: Aframax and partially loaded Suezmax tankers dominate. Fully loaded VLCCs (up to 2 million barrels) are too large for the canal and typically route around the Cape of Good Hope. Suezmax vessels (capacity ~1 million barrels) are sailing partially loaded to meet Panama’s draft and beam restrictions.

Examples include:

Greece-flagged Aframax Sea Turtle (Houston to Yeosu, South Korea).

Liberia-flagged Suezmax Aquahonor (~1 million barrels capacity, to South Korea).

Hong Kong-flagged Suezmax Front Singapore (to Japan).

Types of Crude/Fuel: Light, sweet U.S. grades (e.g., WTI Midland, Eagle Ford blends) from PADD 3. This route carries crude, distinct from the canal’s traditional dominance by refined products (diesel, gasoline, jet fuel, and LPG/LNG).

Overall, Panama Canal petroleum traffic remains ~95% refined products and LNG, but the crude component is surging.

Destinations and Drivers

Asian refiners—particularly in South Korea, Japan, and broader Northeast Asia—are the primary buyers. The Panama Canal offers the shortest, fastest route from the U.S. Gulf Coast to Asia, a critical advantage amid disruptions in traditional Middle East supply chains caused by the U.S.-Israel conflict with Iran and rerouting around the Strait of Hormuz.

This mirrors the broader export boom detailed in our prior coverage: U.S. Gulf Coast crude loadings tracking near 4.9 million bpd in April and projected above 5 million bpd in May—the highest sustained levels on record. Exports represent surplus production after meeting domestic needs, with no strain on U.S. fuel supplies.

Canal Traffic Context

The Panama Canal is operating at full capacity with 36–38 daily transits—above earlier forecasts—driven largely by energy shipments (U.S. crude, LNG, and LPG). Record-high auction fees for priority slots (some exceeding $4 million) and waiting times over three days for unbooked vessels reflect surging demand rather than the drought-related bottlenecks of 2023–2024.

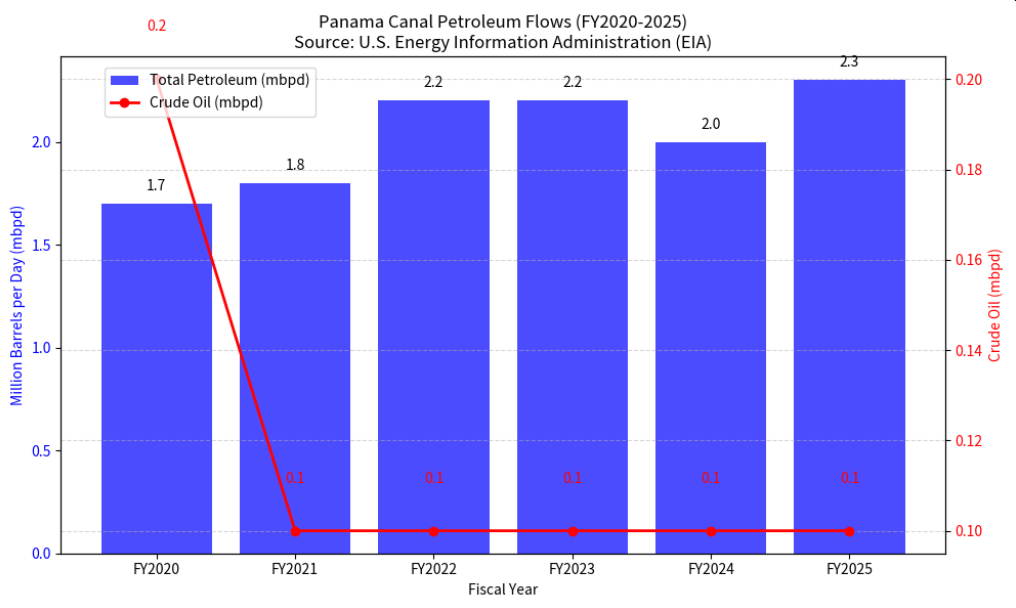

Historical Trends and Charts

The current spike comes after a period of subdued activity during 2023–2024 drought restrictions, when the route saw minimal crude usage. Pre-drought levels were higher, with July 2022 marking a prior peak for U.S. crude via Panama.

For broader context on Panama Canal petroleum movements (the vast majority refined products, with crude a smaller but now-growing share), see the chart below based on U.S. Energy Information Administration (EIA) data:

Chart: Panama Canal Petroleum Flows (FY2020–2025)

Total petroleum (blue bars) has ranged 1.7–2.3 million bpd, with crude oil (red line) historically ~0.1–0.2 mbpd. The 2026 crude surge via U.S. exports pushes the crude component notably higher.

Source: EIA World Oil Transit Chokepoints analysis.U.S. crude exports overall continue their long-term climb (national averages rising from ~3 mbpd in earlier years toward record territory), with Asia gaining share as European and Latin American markets absorb steady refined product flows.Outlook

With Hormuz tensions persisting and Asian demand for reliable non-OPEC+ barrels intact, analysts expect the Panama route to remain elevated. This complements the VLCC-heavy Cape routes for larger parcels while providing speed and flexibility for medium tankers. The U.S. remains the world’s top energy exporter, turning geopolitical volatility into opportunity for Gulf Coast producers, terminals, and the broader energy sector.

No domestic supply risks are evident—exports flow from surplus after U.S. refining needs are fully met.

Appendix: All Sources and Links

- Original ENB Article: “Tanker Fleet Knocking at the Gulf of America, but What Are They Buying and for Whom?” (April 17, 2026) – https://energynewsbeat.co/crude-oil-news/tanker-fleet-knocking-at-the-gulf-of-america-but-what-are-they-buying-and-for-whom/

- Bloomberg: “Oil Tankers Hauling US Crude Via Panama Approaching 4-Year High” (April 17, 2026) – https://www.bloomberg.com/news/articles/2026-04-17/oil-tankers-hauling-us-crude-via-panama-approaching-4-year-high

- Reuters: “US crude heads to Asia via Panama Canal as Iran crisis redraws trade flows” (March 19, 2026) – https://www.reuters.com/business/energy/us-crude-heads-asia-via-panama-canal-iran-crisis-redraws-trade-flows-2026-03-19/

- Gulf News: “Oil, gas tanker traffic explodes at Panama canal as global energy routes shift amid Mideast war” – https://gulfnews.com/business/energy/oil-tanker-traffic-explodes-at-panama-canal-as-global-energy-routes-shift-amid-mideast-war-1.500509612

- U.S. Energy Information Administration (EIA): World Oil Transit Chokepoints (Panama Canal data FY2020–2025) – https://www.eia.gov/international/analysis/special-topics/World_Oil_Transit_Chokepoints

- EIA PADD 3 and U.S. Crude Export Data (historical context) – Various tables referenced in original ENB reporting.

- Kpler Ltd. (tanker tracking and fixture data, cited via Bloomberg/Reuters).

- Panama Canal Authority statistics (transits and tolls) – https://pancanal.com/ and related logistics portals.

Data current as of April 17, 2026. All figures subject to final revisions by reporting agencies.

The post Oil Tankers Hauling US Crude Via Panama Approaching a 4-Year High appeared first on Energy News Beat.