California’s fuel markets are in crisis. Refineries across the state are running flat-out on jet fuel and diesel to chase record-high margins, while gasoline output is being deliberately cut — even as pump prices surge toward all-time highs near $6 per gallon. The shift comes at the worst possible moment: two major refinery closures have slashed in-state capacity by roughly 17–20%, domestic crude production continues its long decline, and the primary overseas supplier region (Asia) is sending far fewer tankers loaded with compliant CARB-grade fuels. The result is a tightening supply picture that analysts warn could push California into summer shortages and even higher prices.

According to the latest data, California refiners boosted CARB-diesel output by 16,000 barrels per day (b/d) and jet fuel by 20,000 b/d in April 2026, while cutting CARB-gasoline production by 32,000 b/d. Gasoline output has averaged around 590,000 b/d — already 20% below year-ago levels — despite still making up roughly half of total refinery runs. Jet fuel production, meanwhile, has climbed above 300,000 b/d as refiners chase crack spreads that now sit more than $35/bbl above gasoline and $20/bbl above diesel.

Refinery Closures Accelerate the Squeeze

The structural problem is shrinking capacity. California had 23 refineries in 2000; today, only 7 remain. 6 have announced they are closing. The latest blows were the November 2025 closure of Phillips 66’s 140,000 b/d Wilmington/Carson complex in Los Angeles and the April 2026 shutdown of Valero’s 145,000 b/d Benicia refinery in the Bay Area.

Together, those plants represented about 17.5% of state refining output.

With fewer plants, operators are simply following the money. Jet-fuel cracks have exploded above $85/bbl amid global Middle East disruptions, while gasoline cracks lag. The reallocation is happening even though jet-fuel inventories have already plunged to 2.6 million barrels — the lowest level since November 2023 and down more than 25% from last year’s peak.

Inbound Tankers from Asia Dry Up

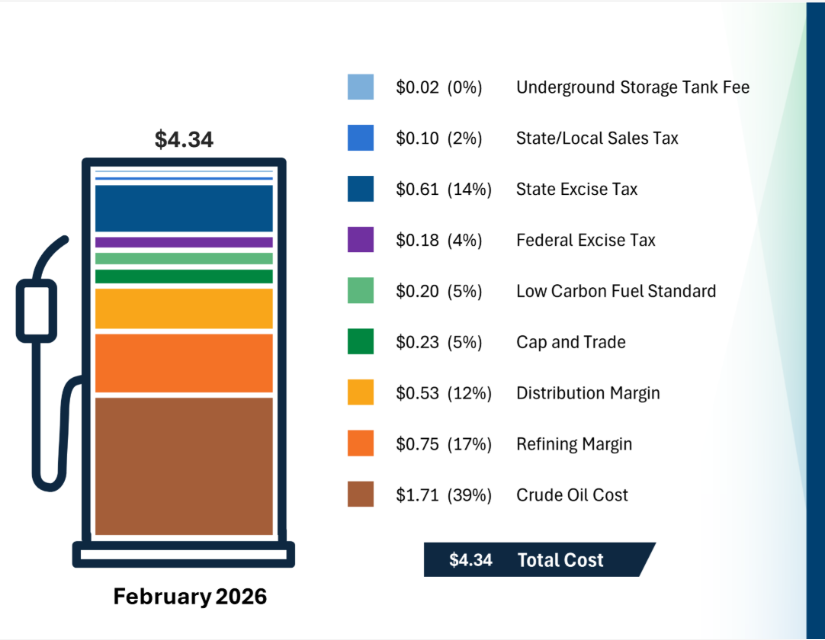

California is a fuel island. It has no inbound pipelines from the rest of the U.S. and must rely on seaborne imports for roughly 30% of its crude and a growing share of finished products. Asia has traditionally supplied the bulk of those barrels — but those flows are now collapsing. Jet-fuel exports from Asia (South Korea, Japan, China) to California have hit decade lows. With only two days left in April 2026, just one confirmed cargo had departed Asia, according to Vortexa data. South Korean loadings, which averaged 40,000 b/d through March, dropped to 17,000 b/d in April.

Gasoline imports have hit records (130,000 b/d in March, with cargoes from India’s Reliance Jamnagar refinery and even the UK), but CARB’s ultra-strict low-sulfur, low-aromatic specifications mean only a handful of global refineries can produce compliant fuel. Diesel imports are also rising, yet the overall tanker pipeline remains thin.

How Bad Could This Get for Consumers?

California’s gasoline demand runs approximately 13.4 billion gallons per year (roughly 874,000 b/d). Local production is now running well below that level even before accounting for the full impact of the latest closures. A 17–20% drop in refining capacity translates to a potential gasoline shortfall on the order of 140,000–170,000 b/d if imports cannot fully offset the loss.

With Asian tanker loadings already down sharply and transit times of 10–34 days, May and June arrivals will reflect the current low export pace. Analysts project that sustained 10–15% supply tightness could drive prices another $1–$2 higher, pushing retail gasoline into the $7–$8 range in some markets this summer. Price elasticity studies suggest a 17% supply reduction can trigger price spikes of 25–30% or more in an isolated market like California.

Jet-fuel stocks at 2.6 million barrels equate to roughly 8–10 days of cover at current burn rates. Airlines are already signaling caution; higher fuel costs will translate directly into elevated airfares and possible flight reductions, threatening summer travel and events such as the 2026 World Cup buildup. Diesel tightness will ripple into trucking and goods transport, adding to inflationary pressure across the state’s economy.

How Gavin Newsom’s Energy Policies Helped Create This Crisis

The current crunch did not appear overnight. Under Governor Gavin Newsom, California has pursued the most aggressive anti-fossil-fuel agenda in the nation. Key policies include:

CARB’s ultra-stringent fuel specifications — among the world’s toughest — limit the pool of global suppliers and raise compliance costs for remaining refiners.

Low-Carbon Fuel Standard (LCFS) and cap-and-trade programs have added tens of cents per gallon in regulatory costs.

A 95% drop in new oil-drilling permits since Newsom took office, slashing in-state crude production and forcing even greater import reliance (now ~61% foreign crude in 2025).

The 2035 gasoline-car phaseout mandate, which signaled to investors that long-term demand would collapse, accelerating refinery closures and discouraging maintenance or upgrades.

Profit-margin caps and minimum-inventory rules (SB X1-2 and AB X2-1) created regulatory uncertainty; the margin-cap rule has since been deprioritized for five years, but the damage to investment confidence was already done.

Industry executives have described the environment as a “25-year tyranny” of regulations that drove refineries from more than 40 in 1991 to just 7–11 today. Recent half-measures — such as SB 237 to allow limited new Kern County drilling and temporary waivers under discussion — are viewed as too little, too late.

Outlook

California is now weighing temporary waivers on CARB specifications to ease import constraints. Longer-term fixes — such as the proposed Western Gateway pipeline (target 2029) — remain years away. Without rapid policy reversals or a swift resolution to global Middle East disruptions, the state faces a summer defined by high prices, potential localized shortages, and painful ripple effects on families, businesses, and travelers.

The Energy News Beat Podcast is interviewing California Assemblyman Stan Ellis about this very issue tomorrow morning, and the video is below.

Appendix: Sources, Links, and Charts

- “California Refineries Max Out Jet Fuel While Gasoline Starves,” OilPrice.com, Natalia Katona, April 29, 2026. https://oilprice.com/Energy/Energy-General/California-Refineries-Max-Out-Jet-Fuel-While-Gasoline-Starves.html

Additional Reporting & Data

- NY Post: “Vacations under threat as California’s oil stockpile hangs on by a thread” (April 27, 2026) https://nypost.com/2026/04/27/us-news/summer-vacations-under-threat-as-californias-oil-stockpile-hangs-on-by-a-thread/

- Fortune: “California’s oil and jet fuel supply is getting slammed…” (April 24, 2026) https://fortune.com/2026/04/24/fuel-shortages-iran-war-spread-california-west-coast-help-years-away/

- Argus Media: “California fuel imports soar after refinery closures” https://www.argusmedia.com/en/news-and-insights/latest-market-news/2819382-california-fuel-imports-soar-after-refinery-closures

- Bloomberg: “California Jet Fuel Imports From Asia Drop to Decade Low” (April 28, 2026) https://www.bloomberg.com/news/articles/2026-04-28/california-jet-fuel-woes-deepen-as-asia-flows-hit-decade-low

- LA Times & CEC data on jet-fuel stocks: https://www.latimes.com/business/story/2026-04-24/california-jet-fuel-inventory-dips-to-two-year-low-as-war-strangles-global-oil-supply

- California Energy Commission – Gasoline Data & Statistics: https://www.energy.ca.gov/data-reports/energy-almanac/transportation-energy/california-gasoline-data-facts-and-statistics (13.4 billion gallons sold in 2024)

- California Policy Center analysis of refinery capacity & demand gap: https://californiapolicycenter.org/one-way-to-avoid-gasoline-lines-in-2026/

- Additional policy background: California Globe, Forbes, American Energy Alliance reports on Newsom-era regulations and refinery exodus.

The post California Refineries Max Out Jet Fuel Slashing Gasoline Production appeared first on Energy News Beat.