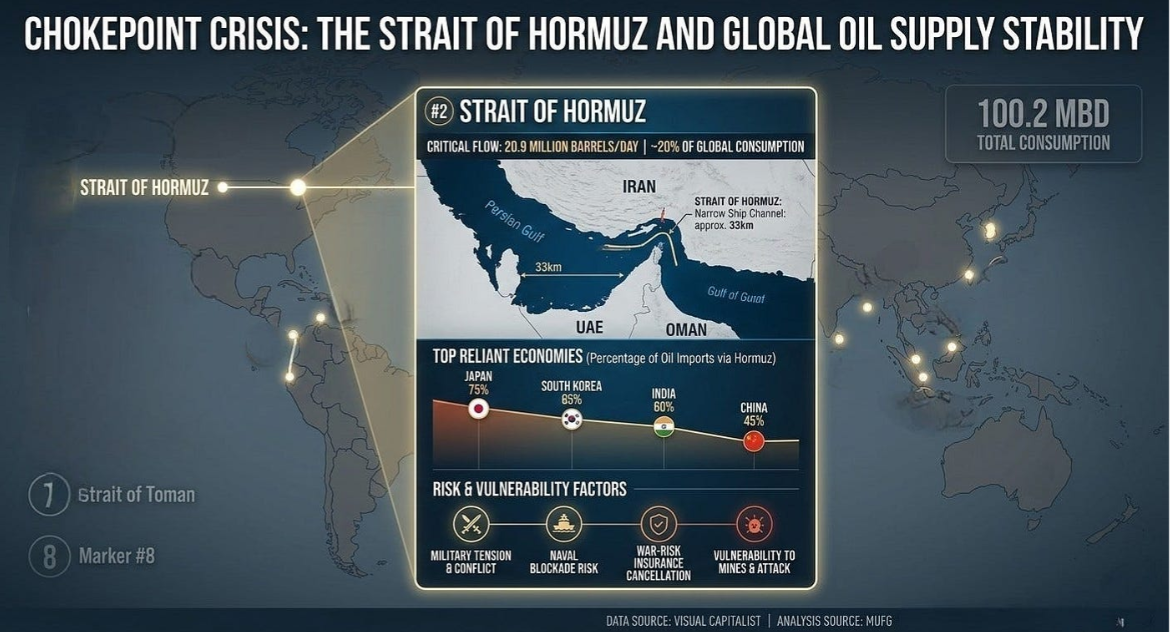

The recent escalation in the Iran conflict — with strikes on energy infrastructure, threats to shipping, and disruptions around the Strait of Hormuz — has done far more than spike oil prices. It has laid bare the world’s true energy demand and the fragility of global supply chains. As Brent crude surged toward and beyond $100 per barrel amid fears of chokepoint closures, markets reacted instantly. The crisis exposed how heavily the world still relies on concentrated fossil fuel flows while highlighting the limits of two decades of massive green energy spending.

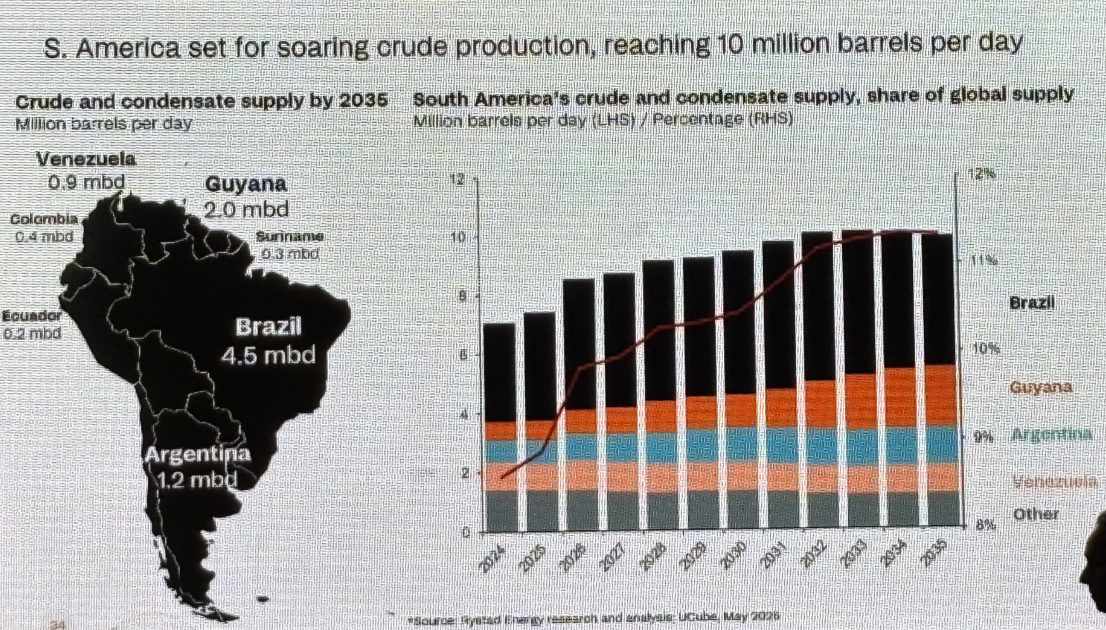

Rystad Energy’s timely analysis, published today, underscores the opportunity this creates. A sustained $100-per-barrel oil price could unlock up to 2.1 million barrels per day (bpd) of additional crude supply from South America by the mid-2030s. This surge would come from offshore developments in Brazil, Guyana, and Suriname (potentially adding over 1 million boepd in the next decade with $33 billion in incremental capex), Venezuela’s low-cost fields (up to 910,000 bpd by 2035), and Argentina’s Vaca Muerta shale (rising from 600,000 bpd today to 1–1.8 million bpd).

As Rystad Senior Vice President Radhika Bansal noted: “The Middle East conflict has done more than spike oil prices — it has exposed how dangerously concentrated global supply chains are around the Strait of Hormuz. South America is now positioned as the world’s most consequential source of incremental supply.” Yet growth depends less on geology than on execution, supply-chain constraints (such as limited FPSO shipyard capacity), infrastructure (like Argentina’s VMOS pipeline), and clear fiscal/regulatory frameworks.

Rystad Energy has repeatedly flagged broader supply chain weaknesses across the global energy sector. In 2026, early softness in oilfield services is giving way to tightening capacity in deepwater, subsea vessels, FPSO fabrication, and offshore rigs. Long lead times for gas turbines, transformers, and critical materials persist, exacerbated by geopolitical risks and competition from both traditional oil and gas and low-carbon projects. The Iran war has only amplified these vulnerabilities, reminding operators that diversified, resilient supply chains are no longer optional.

The Green Energy Reckoning: $10 Trillion for Just 3% of the Mix

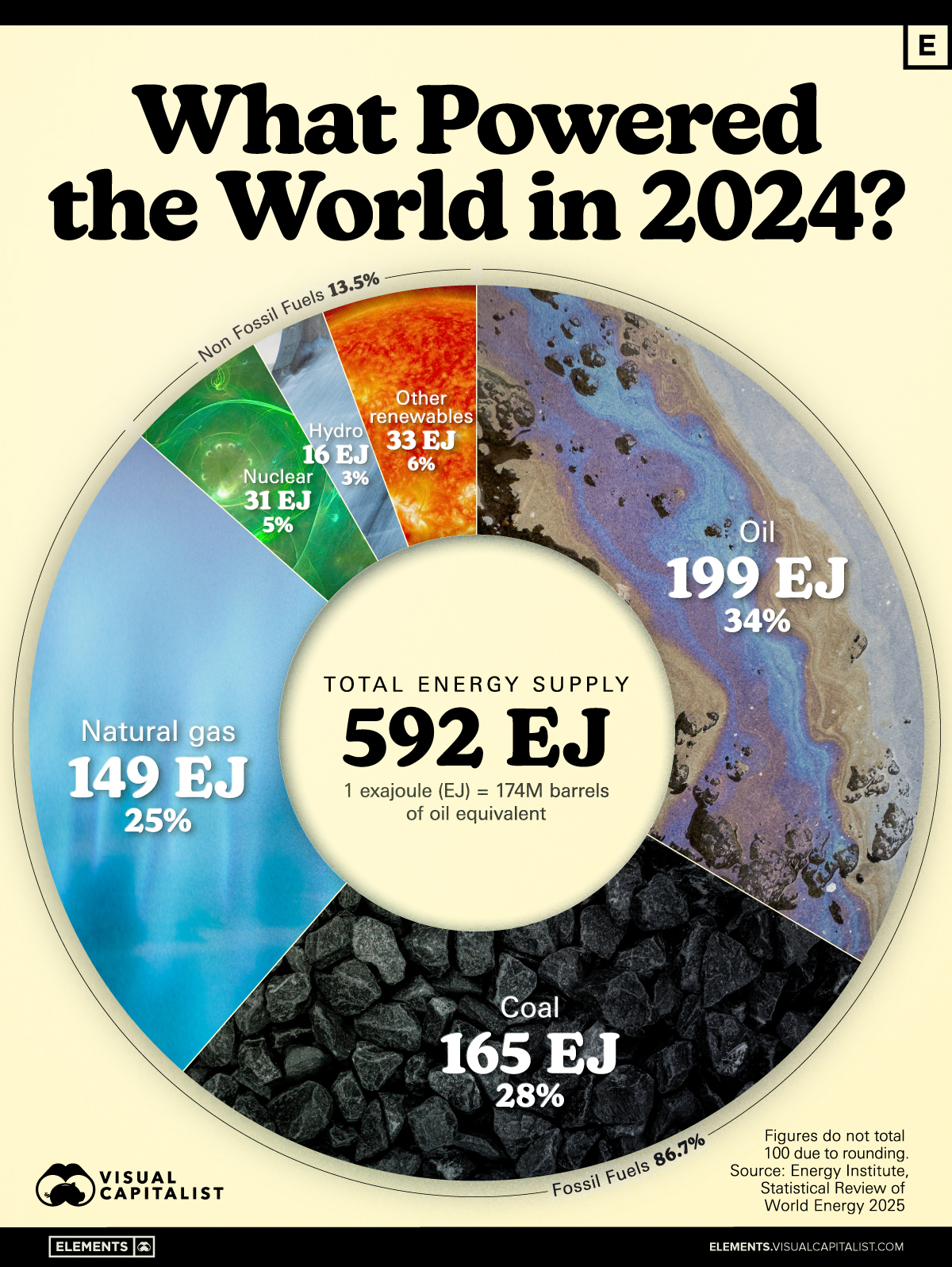

While the conflict drives home the reality of energy demand, it also forces a hard look at the energy transition’s results to date. As U.S. Energy Secretary Chris Wright recently highlighted, the world has poured approximately $10 trillion into green energy over the past two decades — yet wind and solar combined still account for only about 3% of global primary energy.

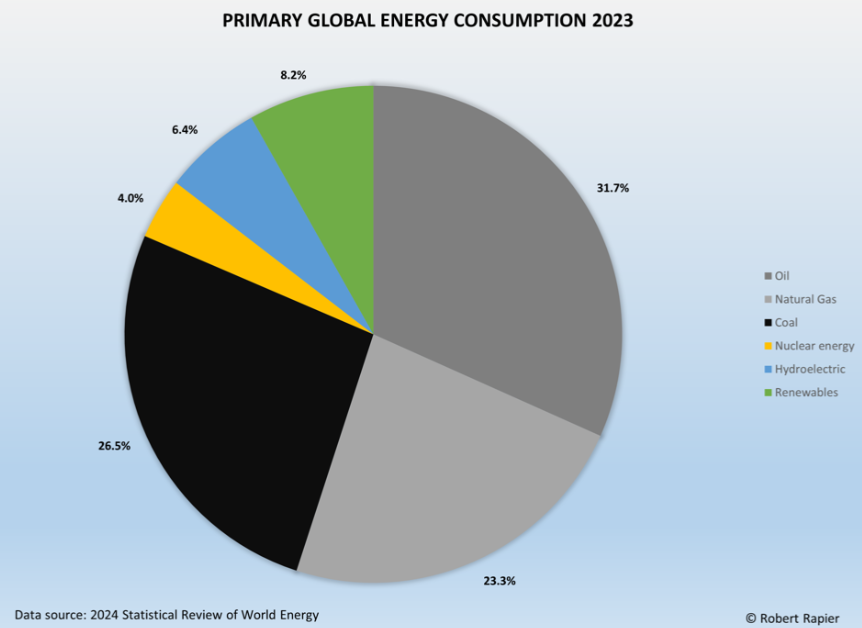

Primary energy data tells the story clearly: Oil (34%), natural gas (25%), and coal (~27%) still dominate the mix, with nuclear and renewables (beyond hydro) contributing far smaller shares in total energy terms. Electricity generation has seen stronger renewable growth (clean sources approaching 40% in power), but primary energy — the full picture of what actually powers the world — remains overwhelmingly fossil-based.

This massive investment has driven up costs in many markets without delivering proportional energy security or abundance. As supply chains for renewables (turbines, panels, batteries, and rare earths) face their own bottlenecks — often tied to concentrated production in China — the limitations become even clearer.The result? A growing consensus that oil, natural gas, coal, and nuclear must remain central as the world redefines energy supply chains. These sources offer dispatchable, high-density power at scale. Nuclear, in particular, is seeing renewed interest globally for its reliability and low-carbon baseload potential.As Energy News Beat Podcast Host Stu Turley has long emphasized: “Energy Security Starts at home, but your energy dominance is displayed through your exports.”

This principle is now guiding pragmatic nations worldwide.

Asia Leads the Charge: Domestic Drilling on the Rise

China, India, and Australia are responding to the exposed vulnerabilities by accelerating local oil and gas exploration and production.

China is pushing record domestic output through its “Seven-Year Action Plan,” targeting sustained oil production around 4 million bpd plus major gas and unconventional gains. Offshore Bohai developments, shale plays, and coal-to-liquids/gas projects are all ramping up to reduce import dependence.

India has launched its largest-ever offshore exploration tender under the Open Acreage Licensing Program (OALP-X), with ONGC committing $18–20 billion to a massive drilling campaign. The goal: cut its ~80–90% oil import reliance and secure domestic supply.

Australia is expanding exploration in frontier basins (including Beetaloo shale and offshore prospects) amid calls to boost local production and address declining conventional output and refining capacity.

These moves reflect a clear strategy: secure energy at home first, then leverage any surplus for regional dominance or exports.

A Tale of Two Approaches: The UK Doubles Down While Others Diversify

In contrast, the UK and a handful of other nations appear determined to double down on green energy as the primary solution. Energy Secretary Ed Miliband has vowed to “double down, not back down” on net zero, accelerating renewables rollout, EV adoption, heat pumps, and solar despite the energy price shocks from the Iran crisis.

Labour frames this as essential for both climate goals and shielding Britain from future geopolitical volatility.

While renewables have a role, the global picture suggests a more balanced, realistic approach is prevailing elsewhere — one that prioritizes reliable, affordable baseload power alongside diversification.

Redefining Energy Supply Chains for the Future

The Iran war has crystallized what many in the energy sector have long understood: true energy security and dominance require pragmatic investment in proven resources, domestic production, and resilient infrastructure. South America’s potential supply surge at higher prices demonstrates the market’s ability to respond when incentives align. Meanwhile, supply-chain realities — from FPSOs to rare earths — demand flexibility, not ideological rigidity.

As the world redefines its energy supply chains in the wake of this crisis, the winners will be those who combine home-grown security with export strength, as Stu Turley aptly put it. Oil, gas, coal, and nuclear aren’t going away — they are becoming more important than ever.

- Rystad Energy / OilPrice.com: “How $100 Oil Could Unleash a South American Supply Surge” (April 21, 2026).

- Rystad Energy reports on 2026 energy supply chain outlook, upstream activity, and geopolitical risks.

- Energy News Beat: “The World Has Spent $10 Trillion on Green Energy — and Only Reached 3% of Global Energy” (recent).

- U.S. Energy Secretary Chris Wright statements via White House Rapid Response.

- IEA World Energy Investment 2025 and related analyses (clean energy investment figures).

- Visual Capitalist / Statistical Review of World Energy data for primary energy mix charts.

- Reuters, Argus Media, and national reports on China, India, and Australia upstream activity (2024–2026 drilling campaigns and tenders).

- UK Government / Ed Miliband statements on net zero policy (April 2026).

- Stu Turley podcasts and statements (Energy News Beat / Conversations in Energy).

- Additional context from CSIS, Forbes, and BloombergNEF on Iran conflict energy market impacts.

Charts sourced from public domain visualizations (Visual Capitalist, Rystad-derived analyses, and industry reports) for illustrative purposes.

The post The Iran War Exposed the Real Energy Demand Around the World appeared first on Energy News Beat.